Solo 401(k) vs SEP IRA

Which Retirement Plan Is Right for Self Employed Business Owners in 2026

If you are self-employed or own a small business, two of the most powerful retirement plans available to you are the Solo 401(k) and the SEP IRA. Both plans allow for high contribution limits and meaningful tax advantages, but they are structured very differently. Understanding how each plan works can help you choose the option that best supports your income, age, tax strategy, and long-term wealth goals.

Below is a comparison of how each plan works, including the 2026 contribution limits.

What Is a Solo 401(k)

A Solo 401(k), also called a one participant 401(k), is designed for a business owner with no employees other than a spouse who earns income from the business. This plan functions much like a traditional employer sponsored 401(k) and allows the business owner to contribute in two roles.

You may contribute as the employee through salary deferrals and as the employer through profit sharing contributions. This dual contribution structure is what makes the Solo 401(k) one of the most powerful retirement savings tools available to self employed individuals. Many Solo 401(k) plans also allow Roth contributions and participant loans, depending on plan design.

What Is a SEP IRA

A SEP IRA, or Simplified Employee Pension, is funded exclusively through employer contributions. There is no employee salary deferral component. Each year, the employer decides whether to contribute and how much to contribute, subject to IRS limits.

If the business has eligible employees, the same contribution percentage must be applied to everyone, including the owner. For solo business owners, this makes the SEP IRA a simple and flexible option, particularly when income fluctuates from year to year.

Under current law, SEP IRAs may also allow Roth contributions. These contributions are made with after tax dollars and grow tax free when qualified distribution rules are met. Availability of the Roth SEP option depends on the plan provider.

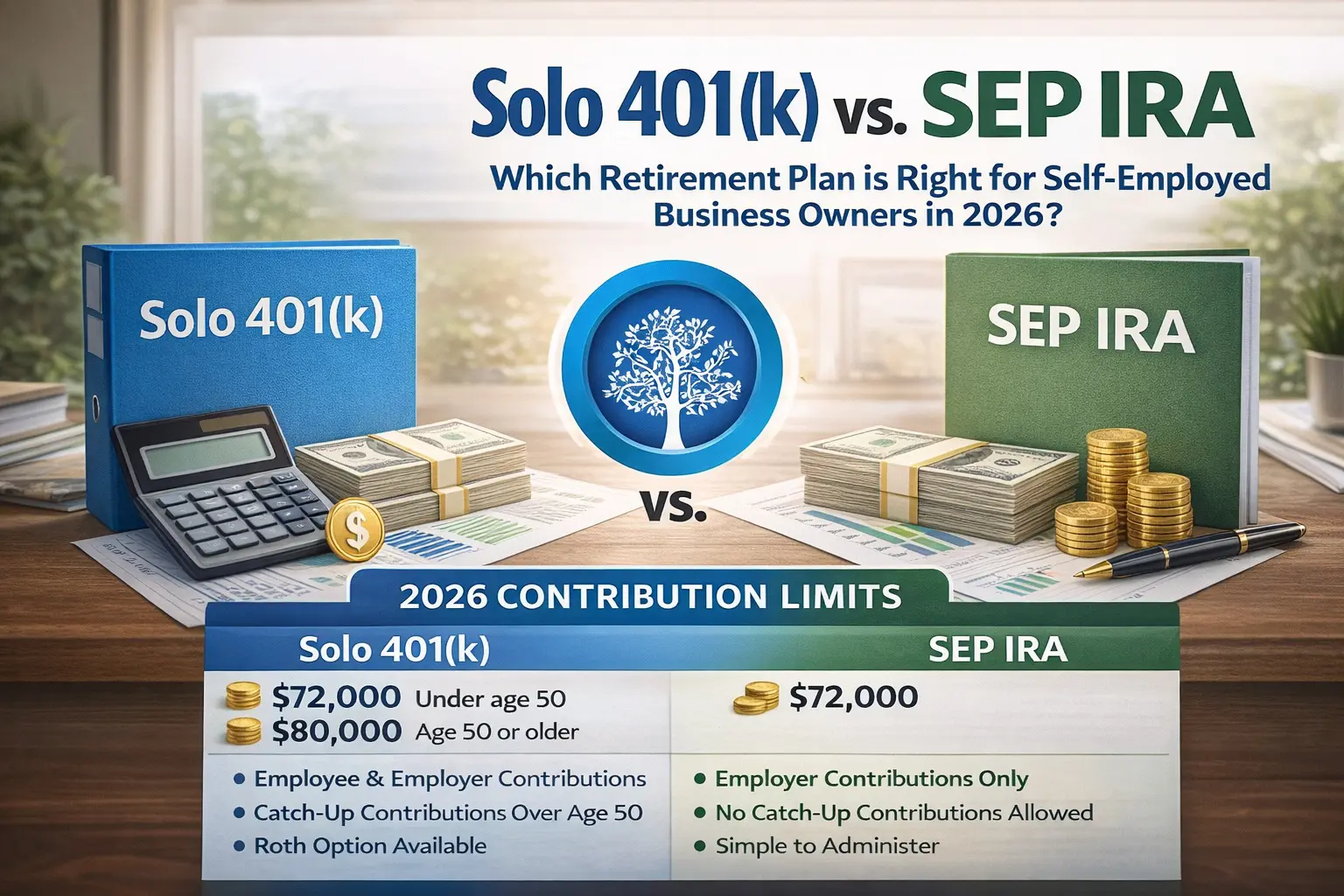

2026 Contribution Limits for Solo 401(k)

For tax year 2026, Solo 401(k) contributions may be made in the following ways.

Employee salary deferrals may be made up to $24,500 for individuals under age 50.

Catch up contributions are available for those age 50 and older. Individuals age 50 to 59 and age 64 and older may contribute an additional $8,000 . Individuals ages 60 through 63 may contribute an enhanced catch up of $11,250.

Employer profit sharing contributions may be made up to 25 percent of compensation.

The total contribution limit for individuals under age 50 is $72,000.

The total contribution limit including standard catch up contributions is $80,000.

The total contribution limit including enhanced catch up contributions for individuals ages 60 through 63 is $83,250.

To make Solo 401(k) contributions for 2026, the plan must be established by December 31, 2026. Employer contributions may be made up to the business tax filing deadline, including extensions.

2026 Contribution Limits for SEP IRA

For tax year 2026, SEP IRA contributions are limited to employer contributions only.

The employer may contribute up to 25 percent of compensation.

The maximum total contribution allowed for 2026 is $72,000.

This limit applies whether contributions are made on a traditional pre tax basis or as Roth SEP contributions.

SEP IRAs do not allow catch up contributions regardless of age.

Special calculation rules apply for self employed individuals when determining allowable contribution amounts.

If the business has eligible employees and the owner elects to make Roth SEP contributions, the same contribution percentage must be applied to all eligible employees.

Key Differences Between a Solo 401(k) and a SEP IRA

A Solo 401(k) allows both employee and employer contributions, while a SEP IRA allows employer contributions only.

A Solo 401(k) permits catch up contributions for individuals age 50 and older, while a SEP IRA does not.

Solo 401(k) plans commonly allow Roth contributions and participant loans, while SEP IRAs may allow Roth contributions but do not permit loans.

SEP IRAs are generally easier to establish and maintain, while Solo 401(k) plans may require additional reporting once plan assets exceed certain thresholds.

Advantages of a Solo 401(k)

A Solo 401(k) offers the highest potential retirement contributions for self employed individuals, particularly those over age 50.

It allows for both pre tax and Roth contributions, providing tax diversification.

It is well suited for business owners who want to maximize retirement savings or who anticipate consistent income.

Advantages of a SEP IRA

A SEP IRA is simple to establish and administer.

It offers flexibility since contributions are discretionary and can change from year to year.

With the availability of Roth SEP contributions, it can also serve business owners who want tax free retirement income without managing a 401(k) plan.

Which Plan Is Right for You

If your goal is to maximize retirement savings, take advantage of catch up contributions, or utilize participant loans, a Solo 401(k) may be the better choice.

If you prefer simplicity, have variable income, or want the option to make employer funded Roth contributions with minimal administrative responsibility, a SEP IRA may be the right fit.

Both plans offer powerful tax advantages and can play a meaningful role in your retirement strategy heading into 2026.

Solo 401(k) vs SEP IRA Comparison Chart for 2026

| Feature | Solo 401(k) | SEP IRA |

| Who It Is For | Self employed business owners with no employees other than a spouse | Self employed individuals and small business owners |

| Employee Contributions | Yes | No |

| Employer Contributions | Yes | Yes |

| Maximum Employee Contribution 2026 | $24,500 | Not allowed |

| Catch Up Contributions | Yes for age 50 and older | Not allowed |

| Catch Up Amount Age 50 to 59 and 64 and Older | $8,000 | Not allowed |

| Enhanced Catch Up Age 60 to 63 | $11,250 | Not allowed |

| Employer Contribution Limit | Up to 25 percent of compensation | Up to 25 percent of compensation |

| Total Contribution Limit Under Age 50 | $72,000 | $72,000 |

| Total Contribution Limit With Catch Up | Up to $83,250 depending on age | $72,000 |

| Roth Contributions | Often available depending on plan | Newly available |

| Participant Loans | Often available | Not available |

| Plan Setup Deadline | Must be established by December 31 of the tax year | Can be established by tax filing deadline including extensions |

| Administrative Complexity | Moderate | Low |

| Annual Filing Requirements | Required once account balance exceeds IRS threshold | None |

| Best For | Maximizing retirement savings and tax strategy | Simplicity and flexible employer contributions |

Contact Us:

Whether you want to invest in real estate, crypto, or private companies, we can help you get started with a self-directed IRA. We’re here to help you stay compliant while you grow your retirement wealth confidently and intelligently.

Call us today at (866) 447-6589

Email us at info@uDirectIRA.com

Book a Call: HERE

Let’s make your retirement investing work for you—not just Wall Street.